Exploding Alberta's "Oil Demand Will Grow Forever" Myth

Economist Peter Tertzakian gets it wrong, but he's got plenty of company

Alberta’s view of oil’s future is driven by politics and narratives, not data, evidence, and rigorous analysis. Sadly, neither is the view of Ottawa and key hydrocarbon provinces like British Columbia and Saskatchewan. The odd bit of economic analysis that does appear in public is shoddy and intellectually lazy. Exhibit A is Peter Tertzakian’s “End of Oil? We’ve Heard that Before.”

The veteran economist argues that forecasts of oil’s decline are narrow, overly focused on road transport, and blind to growing demand from petrochemicals, aviation, and shipping. But his critique rests on the same flaw he attributes to others: untested assumptions. By anchoring his argument in the International Energy Agency’s Current Policies Scenario (CPS), Tertzakian isn’t simplifying; he’s showing his bias. Scenarios are potential futures. Figure in a global energy shock here, a technology disruption there, maybe tightening or loosening of climate policies, and the energy system in 2050 looks very different from one scenario to another.

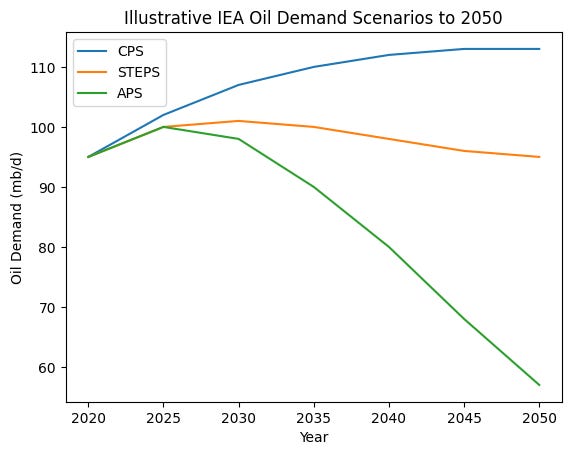

The beauty of energy demand modelling is that it’s based on clearly stated assumptions that can be compared to trends in the data and evidence. That’s what I did in the essay below. OPEC’s well-known modelling was used for the high case instead of the CPS, STEPS was the base case, and APS was the low case. How did they stack up?

You can read the essay for the details, but, in my opinion, APS best fits the trends as we understand them now. Can this change? Of course. Look at how the US-Israel attack on Iran has created a massive shock for the global energy system. Who knows how it will all turn out?

But there is one lesson Canada—and Tertzakian—should acknowledge: the difference between the scenarios is significant. CPS oil demand plateaus at 113 million barrels per day, STEPS falls to 95 million barrels per day, and APS plunges to 57 million barrels per day. That means APS is half of Tertzakian’s confident assertion. And I’ve made the case that APS is far more likely than CPS.

Here’s the scary part: Canadian policymakers make the same mistake as Tertzakian.

I contacted the energy department in British Columbia and Natural Resources Canada in Ottawa and asked which modelling scenarios the respective ministers rely upon for their bullish public comments about the future of oil and gas. The answer was modelling studies conducted by a variety of agencies that were akin to CPS and STEPS. APS, apparently, wasn’t even considered.

Why do economists like Tertzakian and those in the various government departments not pay more attention to the APS scenario and its potentially dire consequences for the Canadian oil and gas industry? I don’t know, but I have a hypothesis.

I interview approximately 500 energy experts every year. Perhaps half of them are Canadian. The other half are located primarily in the United States and Europe, with a mattering in Asia. My observation is that Canadian energy experts, especially economists, simply don't pay much attention to the literature and analysis of the global energy transition. A rich school of theory and study is mostly ignored. The few Canadian economists who are plugged into this work agree with me on this point.

There is an energy revolution going on and, for the most part, Canadian experts have missed it. I count Peter Tertzakian among that group. Here are three points that illustrate my argument.

The CPS Fallacy: Scenario Posed as Reality

Tertzakian’s argument rests on the CPS scenario, which he treats as a neutral baseline rather than what it is: a conditional projection built on specific assumptions about policy inertia and technology uptake. CPS does not describe the future; it describes a world in which governments fail to accelerate electrification and technology adoption proceeds at a measured pace. Those assumptions are already being challenged, particularly in Asia, where the bulk of future oil demand growth is expected.

China, which accounts for roughly 15–16 per cent of global oil consumption, has already seen gasoline demand plateau as EV penetration was 51% in 2025 and is expected to be 55 to 60 per cent of new sales this year. The IEA says Chinese road transport oil consumption peaked last year and total demand will peak before 2030. Chinese modelling shows consumption dropping from 17 million barrels per day now to 6.5 million barrels per day (Sinopec) to 7.5 million barrels (CNPC) per day.

Oil consumption drops rapidly while petrochemical demand grows slowly. Based on electrification trends in the rest of Asia, China’s model is likely to be common. India’s EV sales are growing at more than 30 per cent annually, while Southeast Asia is rapidly scaling solar and battery deployment. These trends directly contradict the slow-transition assumptions embedded in the Current Policies Scenario.

By accepting CPS without testing its inputs, Tertzakian substitutes scenario logic for empirical analysis, making the same error he attributes to oil demand skeptics: mistaking a narrow set of assumptions for reality.

Petrochemicals: The Myth of Unlimited Demand

Tertzakian positions petrochemicals as the engine that replaces lost transportation demand, but he never establishes how large or durable that growth can be. Currently, road transport oil demand is about half of all global oil demand, and petrochemicals account for 12 per cent.

Petrochemical demand is not an open frontier; it is tied to GDP, materials efficiency, and increasingly, recycling and substitution. More importantly, Asia is rapidly expanding capacity, particularly in China, where signs of overbuild are already emerging. At the same time, natural gas liquids are displacing crude as preferred feedstocks in many facilities.

The result is not unconstrained growth, but competition and saturation. Petrochemicals may grow, but not nearly enough to offset structural declines in transport fuel demand.

The Missing Opportunity: Why Not Process at Home?

Tertzakian points to Asia’s refining and petrochemical expansion as justification for exporting Canadian heavy crude, but ignores a critical alternative: processing it domestically.

Alberta already hosts the second-largest petrochemical cluster in North America and has spent years advancing value-added pathways, from asphalt binder proposals led by northern Indigenous cooperatives to carbon fibre derived from bitumen through Alberta Innovates. If petrochemical and materials demand is truly the future, why ship raw feedstock halfway around the world?

The more strategic question is why Canada isn’t capturing that value at home through refining and upgrading, rather than reinforcing its role as a supplier of unprocessed crude.

Narrative Capture: Why Alternatives Are Ignored

The more uncomfortable explanation is that alternatives like domestic upgrading are not seriously examined because much of the energy discourse remains anchored to industry narratives. As is always the case, incumbents like the giant oil sands producers dominate Canada’s public energy discourse.

Economists, analysts, and policymakers often operate within a framework shaped by the oil sector, where exporting raw crude is treated as the default, not a choice to be tested. The same dynamic is visible in Alberta’s policy approach.

When analysis begins with narrative rather than evidence, entire pathways—like building domestic refining and petrochemical capacity—fall out of consideration.

This is not a failure of economics. It is a failure of intellectual independence, and it narrows the range of possible futures.

Collegial Consensus: The Cost of Uniform Thinking

An oil executive once described Alberta’s industry culture during an interview as “collegial consensus.” On the surface, that sounds constructive. In practice, it enforces intellectual conformity. Disagreements are managed privately, behind closed doors, while the public-facing narrative remains tightly aligned.

The consequences are predictable: analysts who challenge the dominant view risk losing access, contracts, or career advancement. Over time, dissent is filtered out, and what remains is a narrow band of acceptable opinion. This is how analysis becomes repetition.

It explains why arguments like Tertzakian’s feel familiar. They reflect a consensus that has already been decided.

Analysis Requires Testing Assumptions

This is not a debate between competing scenarios, where one simply chooses between the IEA’s Current Policies Scenario and more aggressive transition pathways. It is a question of analytical rigour.

In his article, Tertzakian dismisses the oil demand decline argument as narrow, yet he relies on a single scenario and a set of untested sectoral assumptions to support his own claims. That is not a serious engagement with the evidence. It is a selective reading of it.

In this case, the issue is not whether oil demand grows or declines, but whether the assumptions behind either case are examined. On that standard, his argument is thin and unconvincing.

Thank you for bringing facts in a sea of propaganda

Forecasting demand seems to be a fraught business, mostly guided by beliefs (and probably wishes) rather than hard-headed calculations.

I'm worried that the Iran and Russia situations are likely to constrain oil supply and thus spike prices…. Are there things we could do now (or soon) to electrify, so as to be cushioned against the possibility this situation drags on into another year (or two?)? Should individuals be looking at installing solar (wind?) now to protect themselves?

If I recall correctly, the feds gave insulation grants during the ‘70s oil crisis (avoiding the urea disaster, of course). When should we start thinking about this?